The People’s Bank of China drained CNY100 billion from the system on Tuesday via 28-day bond repurchase agreements.

Some CNY183 billion in outstanding paper is set to mature this week. The bank drained a net CNY41 billion from the market last week.

Money market rates have hovered around relatively low levels but may tick up in the coming weeks as corporate income tax is paid into government accounts.

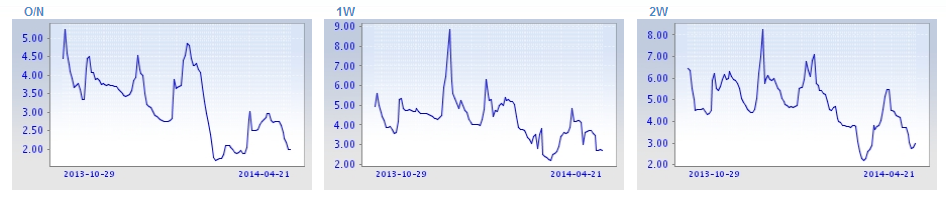

Interbank rates certainly have loosened, a lot:

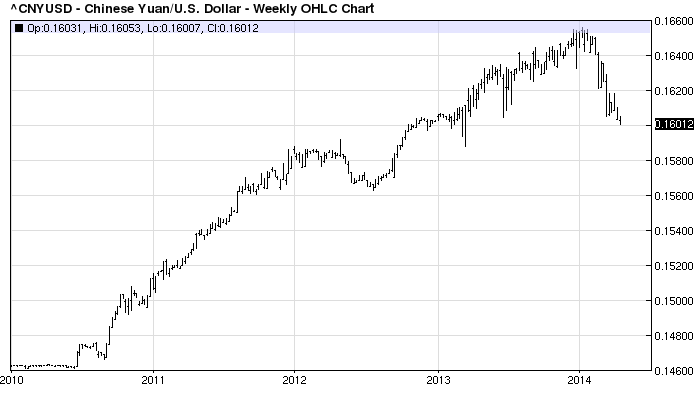

Conversely, the PBOC also set its yuan benchmark at the lowest since September 2013 and the trend to weakness against the US dollar continues:

Advertisement

That ensures hot money flows remain under pressure and will crimp credit in the shadow banking market. But that pressure remains focused on trusts. Demand for wealth management products is still booming (WMP) with interest rates falling across the curve. From Investing in Chinese Stocks:

Interest rates continue to decline with ample liquidity, but investors continue to prefer short-term, guaranteed products from the large banks.

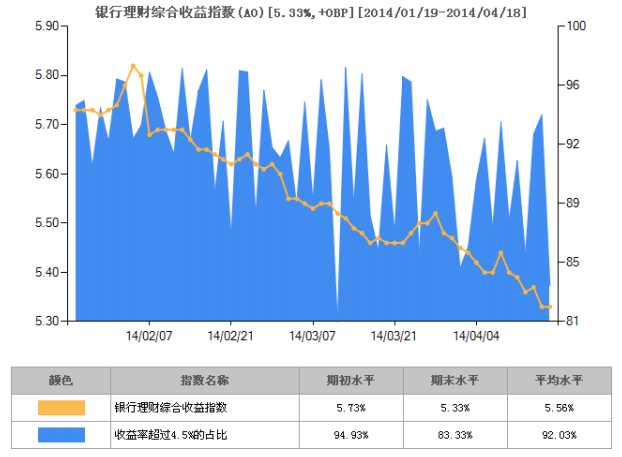

Data from 金牛理财. Total WMP market interest rate (yellow line) with percentage of WMPs offering rates above 4.5%:

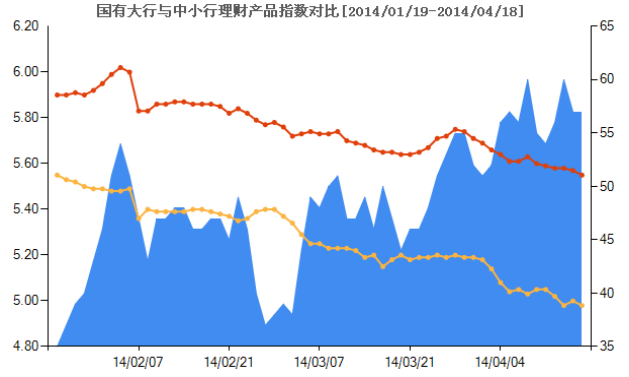

Interest rate on WMPs offered by large (yellow) and medium & small banks (orange), spread in blue:

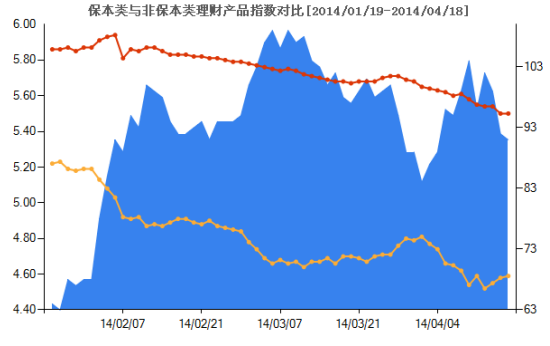

Interest rate on guaranteed WMPs (yellow) and non-guaranteed (orange), spread in blue:

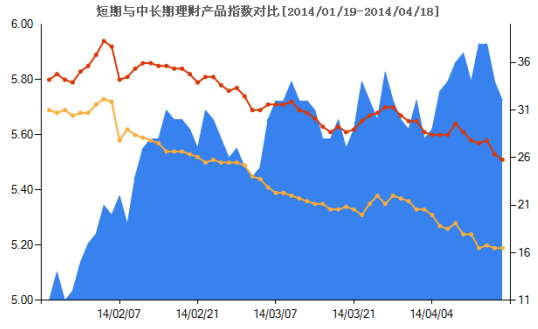

Interest rate on WMPs of short maturity (yellow) and medium/long maturity (orange), spread in blue:

Advertisement

It seems more and more likely that what is actually driving loose interbank markets is a tightening of credit standards and lower lending. The China Securities Journal ran a front page article today beseeching government not to lose its nerve in busting the property bubble. From ForexLive:

The government should not send a signal that it will “save the property market”

Should instead allow adjustments to occur by market mechanisms themselves

Property price cuts, even breaking funding chains for some developers, are part of the process for a bubble to deflate

Even regional collapses of property markets won’t wear down the banking system and large-scale property price declines won’t have a significant impact on banks.

But they will on the interbank market and non banks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.